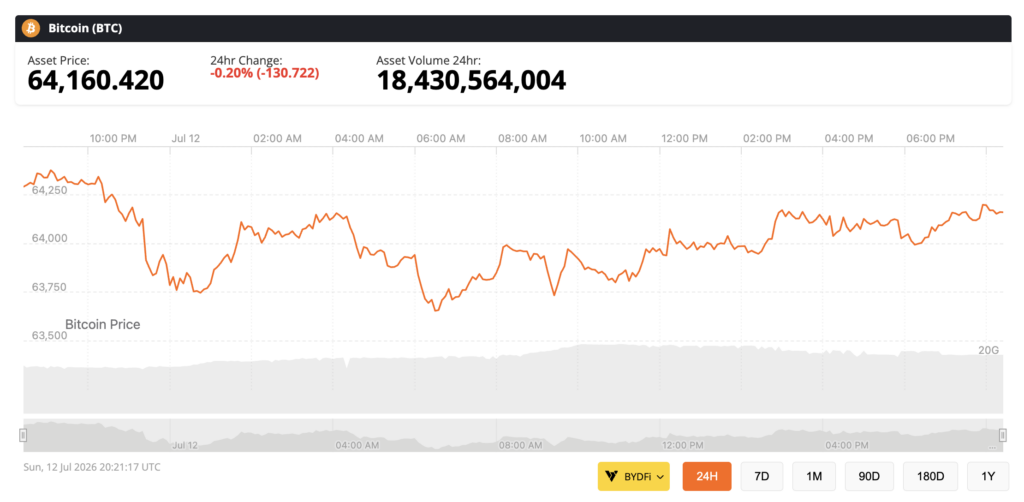

The world’s largest digital asset was trading near $64,160 on Monday, with a market capitalization of roughly $1.29 trillion, according to live market data from Brave New Coin. That is a cleaner setup than the panic conditions seen earlier this month, when Bitcoin broke below $60,000 and Citi cut its 12-month price target.

Bitcoin remains steady, Source: Brave New Coin

The next catalyst arrives Tuesday, when the Bureau of Labor Statistics releases the June Consumer Price Index at 8:30 a.m. ET. The May CPI report showed headline inflation running at 4.2% year over year, while core CPI, excluding food and energy, rose 2.9%. That is not the sort of inflation profile that gives speculative assets an easy ride. It is especially awkward for Bitcoin, because the ETF bid that was supposed to institutionalize the asset now looks more conditional than structural.

The near-term ETF picture has improved. Farside Investors shows U.S. spot Bitcoin ETFs posted $90.4 million of net inflows on July 10, reversing two consecutive daily outflows of $84.9 million and $95.3 million. For the week beginning July 6, the products brought in a net $197.4 million, based on Farside’s daily flow table.

That is useful, but it is not the same thing as conviction. ETF flows have become Bitcoin’s most important marginal demand signal, and the signal is choppy. A week of inflows can steady the tape. It does not erase the fact that professional investors were already reducing exposure before this latest macro test arrived.

A CoinShares 13F report published in June found that professional Bitcoin ETF holdings fell from 313,000 BTC to 261,000 BTC in the first quarter, a 17% decline. The dollar value of those holdings dropped 35% to $17.8 billion, while the share of U.S. Bitcoin ETF assets held by 13F filers declined from 24.7% to 20.8%. Hedge funds and brokerages drove almost all of the reduction. CoinShares analyst Matt Kimmell put it bluntly: “Leveraged and tactical strategies unwind.”

The ETF wrapper made Bitcoin easier to buy, but it also made it easier to sell. The same vehicle that let advisors, banks and hedge funds enter the trade without touching private keys also lets them cut risk with the same indifference they apply to any other line item in a portfolio.

This is why the latest flow rebound should be treated with care. It may be real buying. It may also be positioning ahead of CPI, dealer hedging, or simple mean reversion after a rough stretch. As Brave New Coin noted in its earlier look at Bitcoin ETF holders being in the red, this cycle has already forced ETF investors to confront the less glamorous side of institutional adoption: regulated access does not make drawdowns smaller.

Tuesday’s CPI report matters because Bitcoin is no longer trading only on crypto-native variables. ETF flows, exchange balances and on-chain behavior still matter, but the dominant question is whether the Fed will allow financial conditions to loosen. Right now, the answer is not obvious.

The Fed held its target range for the federal funds rate at 3.50% to 3.75% at its June meeting. The statement said inflation remained elevated relative to the central bank’s 2% goal and pointed to supply shocks, including energy, as part of the pressure. That alone would be enough to keep Bitcoin cautious. The minutes were more important. According to Reuters, nine of 18 policymakers saw rates slightly higher by the end of 2026, and a few participants already saw a case for raising borrowing costs at the June meeting.

That is a very different market from the one crypto bulls prefer to imagine. Bitcoin has spent much of its ETF era being valued as a long-duration risk asset with a monetary debasement story attached. That works beautifully when investors believe rate cuts are coming. It works less beautifully when inflation is sticky, the Fed is discussing rate hikes, and real yields are not being bullied lower by policy makers.

New York Fed President John Williams captured the problem last week when he told Reuters, “Inflation is still too high.” The New York Fed’s June Survey of Consumer Expectations showed one-year inflation expectations rising to 3.7%, the highest reading since September 2023, while three-year expectations rose to 3.3%. The five-year measure stayed at 3%, which is a relief, but not enough to make the Fed dovish by default.

For Bitcoin, the CPI print is not merely another volatility event. It is a referendum on the ETF recovery. A soft print would support the idea that the July inflows are early positioning for a friendlier liquidity regime. A hot print would make the inflows look more like fragile dip buying into a macro wall.

Citi has already moved in that direction. The bank cut its 12-month Bitcoin target to $82,000 from $112,000 and lowered its Ether forecast to $2,240 from $3,175, according to Reuters. The more important part was not the target cut. It was the reason. Citi reduced its 12-month net ETF inflow assumption to zero from $10 billion, citing negative ETF flows, slow progress on U.S. crypto legislation and a rotation into AI-related assets.

That last point deserves more attention. Bitcoin is not just competing with bonds and cash. It is competing with Nvidia, AI infrastructure, private credit, IPOs and any other asset class that can tell a cleaner earnings or productivity story. The ETF made Bitcoin investable for institutions, but it did not make Bitcoin unavoidable.

That is the uncomfortable gap between adoption narrative and market reality. The spot Bitcoin ETFs can attract billions when macro conditions cooperate. They can also bleed assets when the rate outlook turns hostile.

Brave New Coin made the same point after Warsh’s first Fed meeting sent Bitcoin and stocks lower.

The conventional view was that ETFs would mature Bitcoin by bringing in stickier institutional capital. That has happened in part. Advisors remain a relatively stable cohort. Banks have increased exposure. BlackRock’s iShares Bitcoin Trust became a major commercial success, and Brave New Coin previously covered how BlackRock’s Bitcoin ETF became one of the firm’s most profitable products.

But maturity cuts both ways. The more Bitcoin enters traditional portfolios, the more it is judged by traditional portfolio math. If inflation is falling and the Fed is preparing to ease, Bitcoin can look like a scarce monetary asset with ETF demand behind it. If inflation is sticky and the Fed is discussing hikes, Bitcoin looks more like a volatile, non-yielding asset competing for capital against AI equities and cash-like instruments with actual yield.

That is the real story heading into CPI. Bitcoin does not need perfect macro conditions to recover, but it does need macro conditions that allow investors to extend risk. The ETF bid can help, but only if the inflation data stops forcing allocators to ask why they should add Bitcoin when the Fed may still be tightening.

For now, Bitcoin’s $64,000 level is a holding pattern. The ETFs have bought the market time and the CPI will decide whether that time was accumulation or merely a pause before the next repricing.

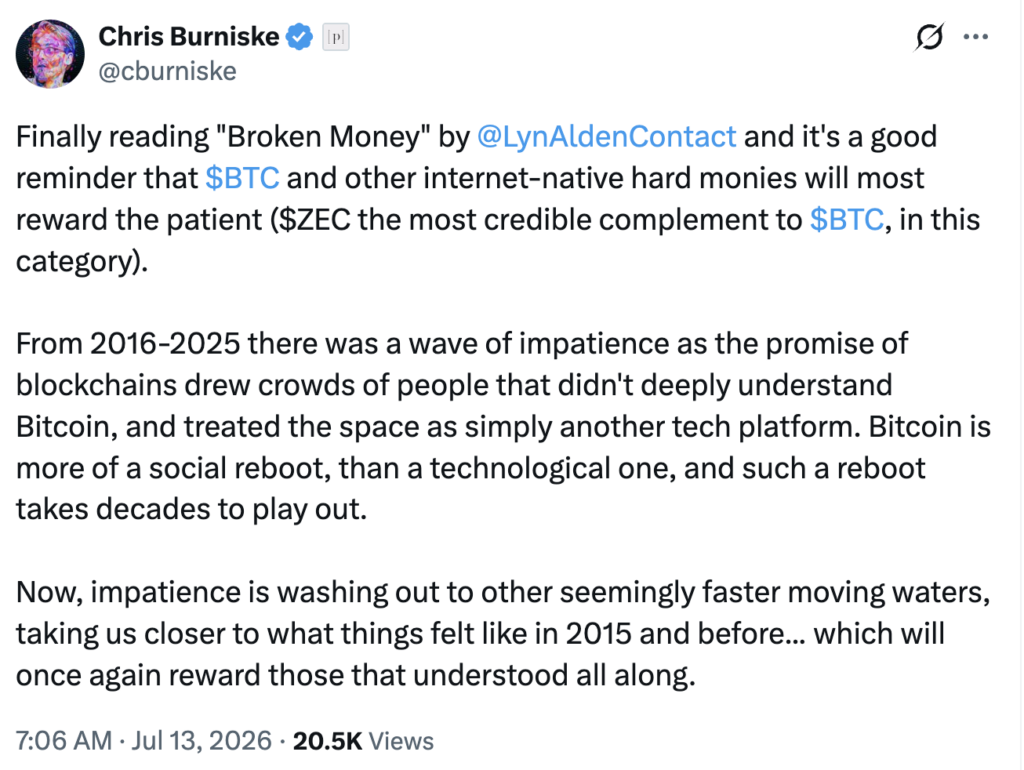

“Impatience is washing out to other seemingly faster-moving waters, taking us closer to what things felt like in 2015 and before… which will once again reward those that understood all along.” source: X

The last word goes to Chris Burniske. His post on X today lands because it captures the mood shift now moving through crypto: the speculative tourists are drifting toward faster-moving narratives, especially AI, while the harder monetary projects are being left to the people with longer time horizons. That does not make Bitcoin, or Zcash by association, suddenly exciting in the short term. It makes them more revealing. If the next phase of crypto looks less like a technology trade and more like a patience trade, then the winners may not be the loudest protocols or the newest platforms, but the assets still standing after impatience has washed out. Give it time.

As analysts have predicted for July based on historical data, BTC is off to a strong start. The leading digital currency has rebounded from its

Traders scanning the order books got a surprise when Altcoin Sherpa expressed bullish sentiment on ETHFI. In a recent tweet, he emphasized the coin’s strong

The strike heightens risks of regional instability, potentially leading to airspace closures and impacting global oil supply routes. The post US strikes hit Ahvaz Airport

Traders are keenly observing ANSEM as it approaches its first significant drawdown. Altcoin Sherpa recently highlighted the importance of monitoring how ANSEM and CASHCAT react