SEC Tokenized Equity Pilot Eyes ATS as Clarity Act Advances The post SEC Seeks Tokenized Equity Pilot as Clarity Act Reaches Senate Floor appeared first

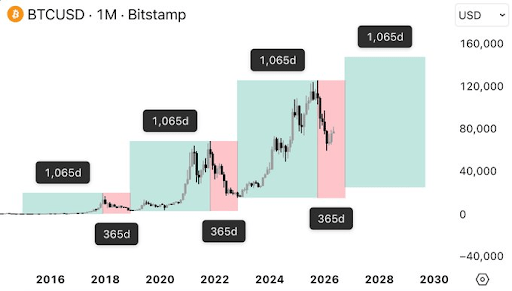

Crypto analyst Cyclop has provided insights into when the Bitcoin price could hit a new all-time high (ATH) above $120,000. This came as the analyst

Armitage’s launch signifies a shift towards more sophisticated DeFi infrastructure, enhancing risk management and yield optimization in crypto lending. The post Wintermute launches Armitage to

Canaan Inc. has been selected to supply hash-to-heat equipment to a district heating network in the Nordic region, deploying its Avalon A1566HA hydro-cooled mining units