Hut 8 is pushing even further into AI infrastructure than most other Bitcoin miners are. Its latest disclosures show a company using power access, data center leases, project debt, and BTC-backed liquidity to build the financing stack for that move.

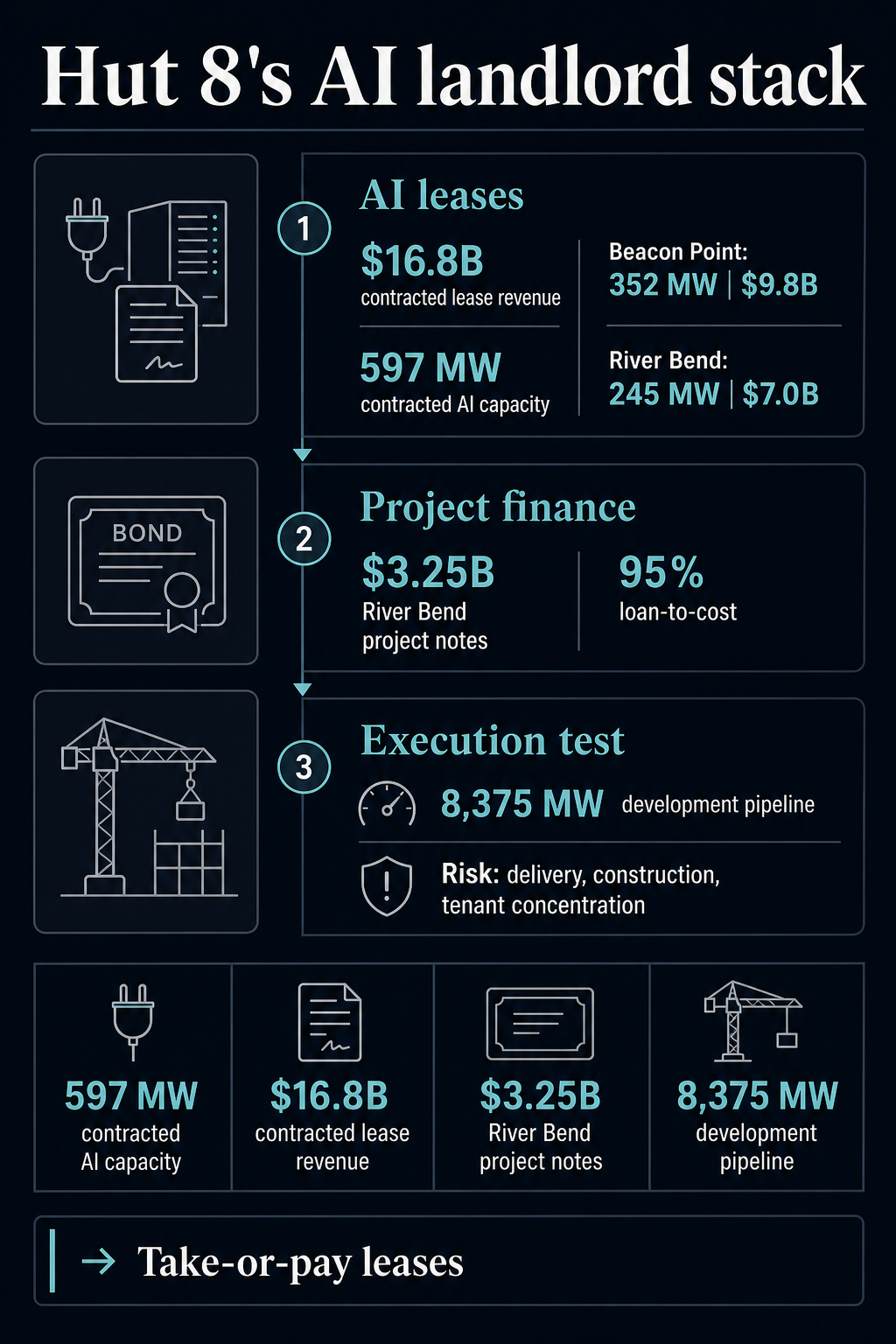

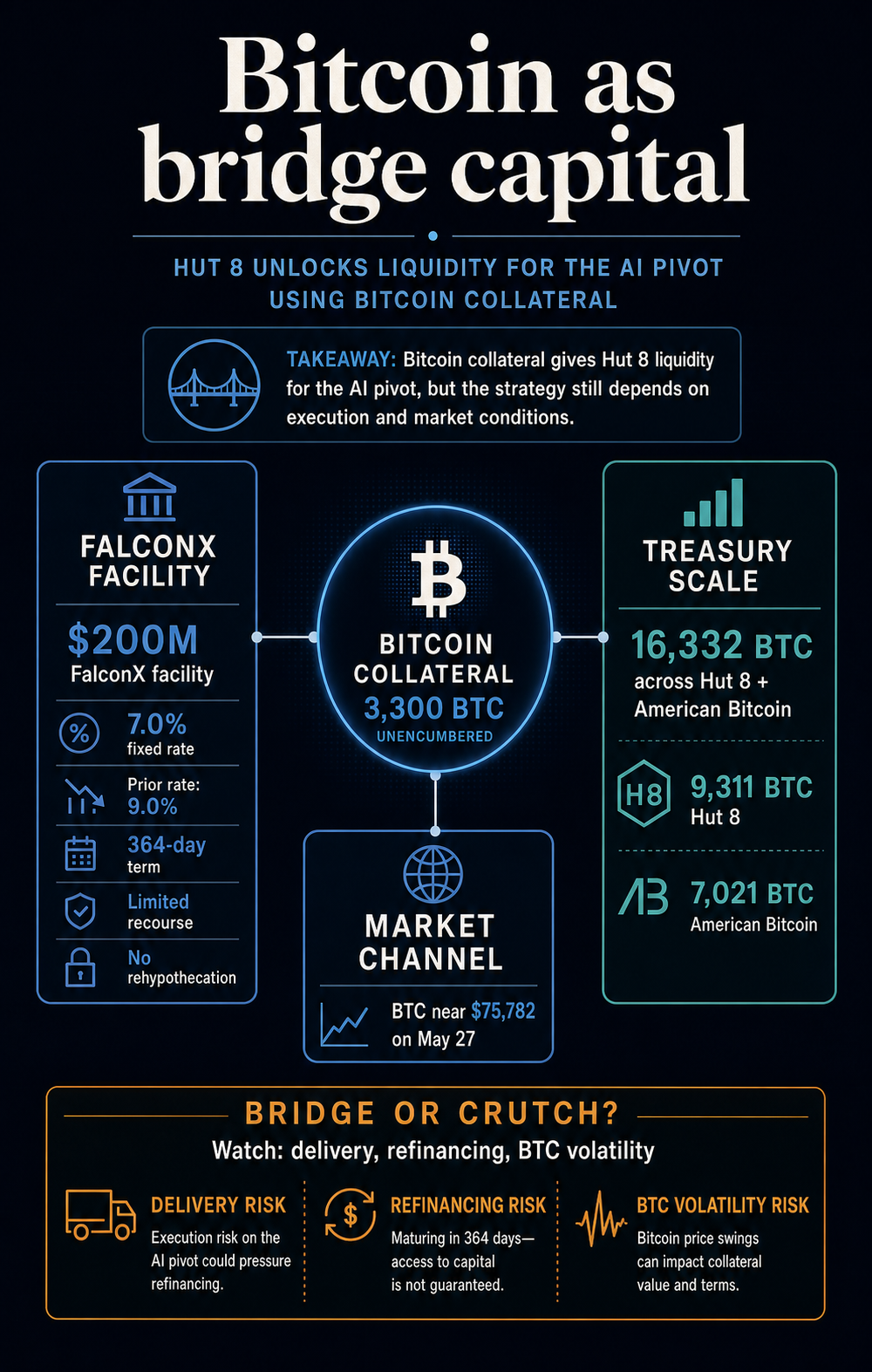

The company’s latest disclosures put numbers around that transition. Hut 8 reported $16.8 billion in triple-net, take-or-pay contracted lease revenue across two hyperscale AI campuses, then separately refinanced a $200 million Bitcoin-backed credit facility with FalconX.

The new facility cut the fixed rate to 7.0% from 9.0% and unencumbered roughly 3,300 BTC from the prior collateral package.

Taken together, the disclosures show a miner identity changing into something closer to an infrastructure landlord. Hut 8 is turning megawatts, lease commitments, project debt, and Bitcoin holdings into the machinery for a business that depends less on mining alone.

The result is a case study with more substance than a generic AI pivot. Hut 8 is showing a funded path into data center infrastructure, though the model still needs operating proof. The test is whether contracted AI cash flows arrive on schedule and become durable enough that Bitcoin collateral becomes a bridge instead of a recurring source of balance-sheet dependence.

The strongest number in Hut 8’s first-quarter disclosure sits outside the Q1 income statement: $16.8 billion of contracted lease revenue across River Bend and Beacon Point, covering 597 MW of AI data center capacity.

Hut 8 generated $71 million of revenue in the first quarter, including $66 million from Compute, and posted a $253 million net loss that included $295 million of primarily unrealized digital-asset losses.

The $16.8 billion figure represents long-term contracted lease value that Hut 8 is presenting as the foundation for a different kind of business.

The pieces are specific. Hut 8’s Beacon Point lease added 352 MW of IT capacity and $9.8 billion of base-term value. Its earlier River Bend lease added 245 MW and $7 billion of base-term value, with Google providing a financial backstop for the base lease term.

Hut 8 is commercializing scarce power and data center capacity under long-term lease structures. The appeal comes from contracts and power access rather than a token, a cloud slogan, or a vague compute promise.

Triple-net and take-or-pay terms are designed to make those cash flows more financeable because the tenant obligation is less tied to day-to-day mining economics.

Hut 8’s disclosures line up across four moving parts:

| Model component | Hut 8 evidence | Reader impact | Risk still live |

|---|---|---|---|

| Power and sites | 597 MW of contracted AI data center capacity across two campuses | Turns miner infrastructure into leaseable digital infrastructure | Delivery, interconnection, construction, and tenant concentration |

| Contracted demand | $16.8 billion in base-term contracted lease revenue | Creates a financing story beyond hashprice exposure | Lease value depends on execution over long timelines |

| Project finance | $3.25 billion River Bend notes, non-recourse to Hut 8 | Reduces the need to fund all growth from equity or BTC sales | Large projects still carry cost, schedule, and market risks |

| Bitcoin balance sheet | $200 million FalconX BTC-backed facility and 3,300 BTC unencumbered | Gives liquidity without immediately selling coins | Collateral value still moves with BTC |

Hut 8’s AI transition has more to it than most, but each component still carries a different kind of risk.

The leases reduce some revenue uncertainty. The bond financing reduces some parent-level funding pressure. The Bitcoin facility improves liquidity. Still, all three leave Hut 8 with the task of building, delivering, and operating infrastructure for customers whose requirements differ from Bitcoin mining.

The FalconX refinancing is the clearest sign that Bitcoin is becoming part of the financing machinery rather than only the asset being mined.

The full Hut 8 release distributed through Nasdaq described the facility as a 364-day Bitcoin-backed loan with limited recourse to pledged BTC, a no-rehypothecation covenant, fixed loan-to-value thresholds, and no loan-to-value ratchet triggered by declines in Bitcoin’s price.

Those terms blunt part of the obvious criticism. The deal improves the terms of a miner’s coin-backed borrowing instead of worsening them to chase a new market.

Hut 8 lowered its fixed cost of debt by 200 basis points and increased Bitcoin held outside collateral covenants. The release valued the newly unencumbered coins at roughly $260 million as of May 1, 2026, giving Hut 8 more balance-sheet room without selling the asset.

That makes the facility a better tool, but not a risk-free one.

Hut 8’s own balance sheet shows why the distinction is important. Its 10-Q said the company held about 16,332 BTC as of March 31, 2026, including about 9,311 BTC held by Hut 8 and about 7,021 BTC held by American Bitcoin.

The aggregate fair value was about $1.11 billion, based on approximately $68,222 per BTC. The same filing tied the first-quarter digital-asset loss to Bitcoin’s decline during the period.

Today, Bitcoin trades near $75,782 on CryptoSlate’s price page, down 2.1% over 24 hours and roughly 40% below its October 2025 all-time high. The market-price channel is the relevant risk.

Bitcoin can provide liquidity without a sale, but the borrowing value, covenant comfort, and refinancing backdrop still depend on the asset’s market behavior.

That is why the AI landlord strategy cannot be separated from the Bitcoin treasury strategy. If AI leases produce reliable cash flows, BTC collateral can be transitional capital. If delivery slips, financing markets tighten, or Bitcoin weakens at the wrong time, the same collateral can keep the pivot tied to the volatility it was meant to escape.

Earlier coverage of miners’ AI pivot showed the broader identity split facing the sector. Miners are moving toward AI and high-performance computing because power access, cooling infrastructure, land, interconnection work, and industrial operations can be worth more under contracted dollar revenue than under compressed mining margins.

Hut 8 fits that broader sector shift. Public miners built businesses around converting power into BTC, and AI data center demand is now giving some of them a second possible use for the same physical footprint.

The difference is that AI customers do not buy the same thing the Bitcoin network buys. Mining can tolerate interruption when economics or grid conditions change. AI tenants want uptime, delivery certainty, dense power, cooling, network architecture, and creditworthy execution.

A miner with megawatts still has to become a hyperscale landlord. It has to turn a power position into infrastructure that lenders and tenants will treat as dependable.

Hut 8’s disclosures show both sides of that transition. The company describes itself as an energy infrastructure platform integrating power, digital infrastructure, and compute. It also still reports digital-asset losses, BTC holdings, and exposure to mining economics.

Some Compute revenue and BTC holdings are held by American Bitcoin, a consolidated subsidiary, making Hut 8’s strategy less straightforward than a clean exit from mining.

That complexity is part of the shift. The market is watching whether miners can stop being pure BTC proxies without losing the balance-sheet optionality that made their treasuries valuable in the first place.

The strongest argument in Hut 8’s favor is that the AI pivot uses more than Bitcoin-backed debt. The company said it closed $3.25 billion of fully amortizing 16.5-year investment-grade senior secured notes to finance River Bend.

Hut 8 described the financing as non-dilutive and non-recourse to Hut 8, with loan-to-cost increasing to about 95%.

That weakens the crutch argument. If project-level debt funds the campus and long-term leases support the debt, then Bitcoin collateral is one part of the structure rather than the whole. It is a liquidity tool alongside project finance and contracted revenue.

The caution is that the financial structure still has to become operationally sound. River Bend is still advancing toward delivery, Beacon Point still has to be built out, and the company still has to convert an 8,375 MW development pipeline into real contracted capacity.

Hut 8 also warned investors about risks tied to data center construction, financing, power expansion, permitting, supply chains, technical challenges, and market conditions.

Hut 8 is showing that miners can finance a route into AI infrastructure when they have scarce power, credible tenants, project-finance access, and a Bitcoin balance sheet lenders will underwrite. It has yet to show that the route is self-sustaining.

The next test is whether AI infrastructure cash flows become strong enough to push Bitcoin collateral into the background. If they do, Hut 8’s BTC-backed financing will look like bridge capital for a miner that successfully monetized its power footprint.

If they fail to do so, the pivot will remain tethered to the same balance-sheet asset that made the strategy possible in the first place.

The post Hut 8 AI landlord data center strategy turns Bitcoin collateral into bridge capital appeared first on CryptoSlate.

Music v2 brings genre-shifting and section-by-section composition to ElevenLabs. Stable Audio 3.0 ships open weights and six-minute tracks. Is either good enough to dethrone the

Binance co-CEO Yi He has become the first crypto-native executive ever named to Fortune’s Most Powerful Women in Business list. The 2026 ranking placed her

SpaceX’s ambitious IPO plans could reshape market dynamics, influencing investor confidence and setting new benchmarks in the aerospace sector. The post SpaceX targets $75B IPO

The SpaceX IPO hype signals a growing convergence of space and digital asset economies, potentially reshaping investment strategies. The post SpaceX IPO hype boosts US