When Robinhood announced it was launching a blockchain, my first reaction was skepticism.

Another brokerage is trying to plant a flag in crypto. Another L2 that would generate headlines for a week and then fade into the background noise of a space that has seen this story play out too many times already. Then the first-day numbers came in, and I had to stop and look twice.

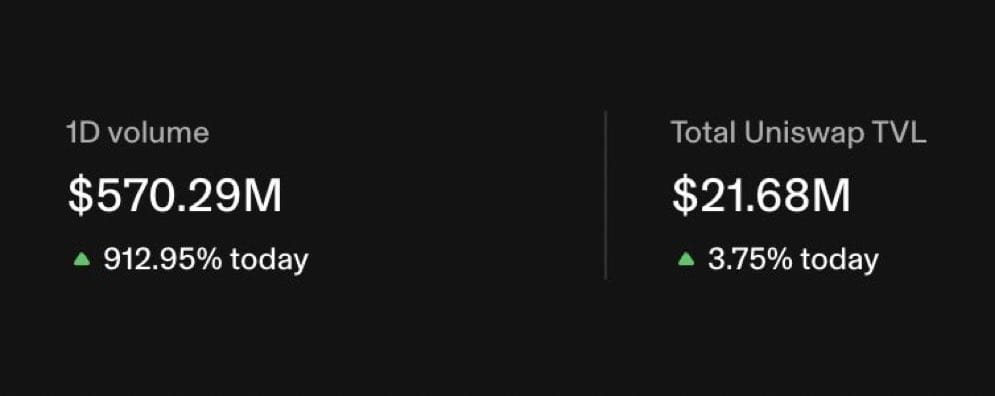

Robinhood Chain posted $570 million in daily volume against just $21.68 million in total value locked. That’s a 26:1 ratio. For context, most established DEXs, the ones that have been running for years and have deep, battle-tested liquidity, sit at or below 1:1. Robinhood Chain turned its entire liquidity base over 26 times in a single day. TVL has already climbed past $240 million since launch, with Morpho and Ethena driving most of that figure. ARB jumped over 12% on the news. And suddenly the skepticism I walked in with started to feel a little less certain.

Robinhood’s crypto team confirmed the chain is live, with bridging already active from Solana, Ethereum, and Arbitrum directly through Robinhood Wallet. You can already add it in Rabby right now.

Announced on July 1, Robinhood Chain is a permissionless Layer 2 built on Arbitrum Orbit. That means it inherits Ethereum’s security while running with the speed and cost structure of a modern L2, not a sidechain compromise, not a proprietary network that asks you to trust Robinhood’s validators. The mainnet is already live, not in testnet, not in preview.

The focus is tokenized stocks and real-world assets alongside what Robinhood is calling an integrated financial experience, DeFi and TradFi in the same environment rather than asking users to choose one world or the other. AI agent support is baked into the infrastructure from day one, with fees covered by the chain for the first 90 days. That subsidy matters for developers who want to build agentic applications without absorbing gas costs while they’re still figuring out whether the chain has the user base to justify the investment.

I’ve seen a lot of L2 pitches. The combination of tokenized equity exposure, DeFi lending infrastructure, and AI agent support in a single environment is new. But what actually sets this apart from every other pitch I’ve read is the distribution number sitting behind it: 28 million funded Robinhood accounts. Most new chains have to fight for every wallet. Robinhood already has 28 million people who have put real money into a Robinhood account. That’s not a potential user base. That’s a waiting room.

Jeffrey Crypto flagged the volume-to-TVL data and it stopped me in my tracks when I saw it broken down properly. A 26:1 ratio on day one is extraordinary by any measure. It’s also, if I’m being realistic, almost certainly driven heavily by speculative and memecoin trading in the earliest hours of a new chain’s life. That’s not a criticism unique to Robinhood Chain, it’s the documented playbook of every major L2 launch over the past two years.

Base did it. Blast did it. Scroll and Mode both did it. The pattern is always the same: big launch, memecoin rush, attention floods in, volume spikes, and then within two to three weeks the speculation moves on and the chain is left with whatever was actually building underneath the noise. The volume drops sharply, the headlines stop, and the real test begins.

I’m not pretending that won’t happen here too. Some version of it almost certainly will. The memecoin traders who showed up on day one are not the long-term users Robinhood is building for, and their volume will fade when the next shiny chain captures their attention.

But here is the thing that keeps me from writing this off the way I’d write off a typical L2 launch: the floor. When Base’s memecoin volume cleared, what remained was a Coinbase-backed chain with genuine developer activity and a growing user base. When Robinhood Chain’s speculative volume clears, what remains is 95 tradeable stock tokens, a zero-fee stock-token DEX built by the dYdX team, a lending product offering approximately 7% APY with Lloyd’s of London insurance on smart contract risk, and 28 million funded accounts sitting one bridge away. No previous L2 launch had any of that waiting underneath the speculation. That’s what makes this one genuinely different to think about, even if the early volume pattern looks familiar.

The 12% ARB surge isn’t just excitement about a new chain launching on Arbitrum’s stack. There’s a structural reason behind it that I think is worth sitting with. Offchain Labs co-founder Steven Goldfeder announced that 10% of fees from Robinhood Chain and all other Arbitrum L2s will flow directly to the Arbitrum ecosystem, 8% into the tokenholder-controlled treasury, 2% into development funding.

That’s not a vague promise about ecosystem alignment. That’s a direct, ongoing revenue stream flowing to ARB holders from every transaction Robinhood Chain processes. Arbitrum One already sends 100% of its fees to the treasury. The Robinhood Chain integration adds a new channel with a retail distribution angle that nothing else in the Arbitrum ecosystem currently has.

What this means for ARB is something I find genuinely interesting from a structural standpoint. It shifts the token from being purely a governance instrument, which is how most L2 tokens get categorized and why they trade at persistent discounts to expectations, toward something closer to a fee-bearing asset. The 8% treasury shares compounds if Robinhood Chain volume scales. That capital can be deployed into grants, buybacks, or staking rewards depending on what governance decides. The revenue is real. What the DAO does with it is where the actual value either crystallizes or gets wasted. That’s the variable I’d be watching most closely if I held ARB.

I want to be clear about something. The memecoin angle is not the thesis here. It’s the noise that shows up on launch day because that’s what always shows up on launch day. The actual thesis is more specific and considerably more interesting.

Robinhood Chain is built specifically to host tokenized equities, stock tokens representing real-world assets, on a permissionless blockchain with a zero-fee DEX designed from the ground up for that asset class by the dYdX team. This is not a general-purpose chain that added stock tokens as a marketing feature. The chain’s primary architecture was designed around this use case, and that distinction matters when you’re thinking about whether the infrastructure can actually support the activity it’s promising.

The lending product sitting alongside it is the part that caught my attention most on a second read. Approximately 7% APY with Lloyd’s of London insurance coverage on smart contract risk is not a typical DeFi yield pitch. Lloyd’s coverage means a real-world insurer has underwritten the smart contract risk, which is the kind of risk mitigation layer that has historically been the missing piece preventing more conservative capital from entering DeFi at all. Morpho and Ethena are already providing the lending market infrastructure, and the data already shows that liquidity is flowing in.

The type of user that 7% APY with insurance attracts is completely different from the memecoin trader whose volume will fade. It’s the Robinhood account holder who has $50,000 in their brokerage and wants yield on tokenized equities they already understand. That user doesn’t need to be educated about blockchain. They need a reason to bridge, and a familiar brand offering a better yield than their money market fund with insured smart contract coverage is a reason that makes sense in the language they already speak.

Here’s where I land on this. The 26:1 volume ratio is a launch-day number. The $240 million TVL is an early-day figure. The 12% ARB move is a reaction to an announcement. Every one of these numbers will look different in a month, and some of them will look significantly smaller.

What I’m watching instead is whether real behavioral change starts to show up. Not speculation volume, not airdrop farmers, not the traders who show up on every new chain for the first week. I’m watching whether Robinhood account holders, people who have never touched a blockchain in their life, who don’t know what a gas fee is, who think DeFi is something that happens to other people, start bridging assets to earn yield on stock tokens through infrastructure that carries a brand name they already trust.

If that happens even at a fraction of the scale the 28 million account number implies, the floor underneath Robinhood Chain’s early volume is categorically different from anything the L2 space has seen before. If it doesn’t happen, this becomes another chart that looked exciting in the first week and then tells a familiar story from week two onward.

I think the honest answer is that nobody knows yet. But I also think the structure here is more interesting than any L2 launch I’ve written about in the past two years. The next month will tell most of the story, and I’ll be watching it closely.

Disclosure: This is not trading or investment advice. Always do your research before buying any cryptocurrency or investing in any services. Follow us on X @nulltxnews

XRP trades near $1.10 as hedge funds pile into yen shorts at 2007 extremes. Can Japanese retail demand fuel a comeback toward $2.00? Key levels,

Bitpanda has opened access to margin trading on real stocks, ETFs, and ETCs in Europe, giving active traders a new way to take short-term positions

EMURGO said it is stepping down from its role in Pentad, the five-member group coordinating Cardano’s infrastructure funding, to focus resources on recovering funds lost

Stablecoins are useful, but crypto still has a simple payment problem: users do not want to think about gas. BNB Chain’s push toward gas-free stablecoin