Stablecoins were built on the premise that removing intermediaries between sender and recipient would erode the relevance of legacy payment networks, but the fastest-growing consumer stablecoin product depends entirely on one.

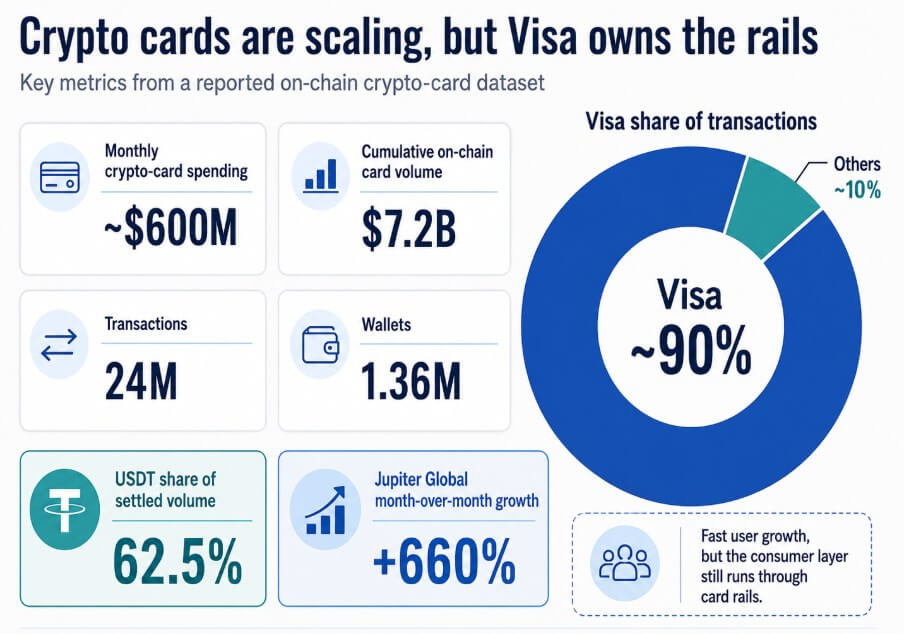

Data reported by The Kobeissi Letter shows crypto-card spending reached roughly $600 million per month, with $7.2 billion in cumulative on-chain card volume across 24 million transactions and 1.36 million wallets.

Approximately 90% of those transactions were processed through Visa, with USDT accounting for 62.5% of settled volume. Jupiter Global, whose USDC-backed card runs on Visa rails, grew 660% month-over-month in the same dataset.

Jupiter Card is a Visa debit card backed by a user’s USDC balance, accepted wherever Visa is accepted. Users deposit USDC, which converts into US dollars behind the card, and merchants receive ordinary fiat, with the blockchain never touching the point of sale.

Bridge-enabled stablecoin-linked Visa cards went live in 18 countries in March, with planned expansion to more than 100 countries by year-end, covering 175 million Visa merchant locations. Phantom and MetaMask are among the crypto platforms already distributing cards of this type.

Visa’s stablecoin settlement pilot separately hit a $7 billion annualized run rate as of Apr. 29, up 50% quarter-over-quarter and now operating across nine blockchains, still a rounding error against Visa’s FY2025 volume of $14.2 trillion, but moving fast enough to show direction.

Stablecoins expand the pool of balances that can fund the card network at checkout, leaving the acceptance layer untouched.

Visa’s durable assets include merchant acceptance across over 175 million locations, embedded compliance relationships, fraud tooling, chargeback infrastructure, and consumer behavior trained over decades.

What Visa lacked was a way to tap into crypto-native wallet balances without forcing users out of their familiar UX or merchants to accept new payment methods, and crypto cards solve that problem cleanly for Visa.

For the original pitch that stablecoins would route consumers around card rails, as crypto did with correspondent banks for cross-border transfers, this outcome is the uncomfortable version.

Holding USDC and tapping Visa converts stablecoin balances into spendable money at scale, but Visa still sits between the user’s dollar-denominated wallet and the merchant, capturing interchange, data, and the consumer relationship at every transaction.

McKinsey estimates B2B stablecoin payments at around $226 billion annually, roughly 60% of global stablecoin payment volume, while stablecoin-linked card spending reached $4.5 billion in 2025, up 673% from 2024.

A Colombian supplier pays in USDC, settling entirely on-chain, while a consumer buying coffee routes through a Visa terminal. Stablecoins damage bank prefunding, FX intermediaries, and correspondent banking far more directly.

| Layer | Stablecoin impact | Who is most exposed | Who benefits |

|---|---|---|---|

| Consumer checkout | Stablecoins stay hidden behind card UX | Direct crypto payment apps | Visa, Mastercard |

| Merchant acceptance | Merchants do not need to accept USDC/USDT directly | Crypto-native POS systems | Existing card networks |

| Cross-border settlement | Faster, cheaper dollar movement | Correspondent banks, remittance intermediaries | Stablecoin issuers, wallets, fintechs |

| Bank deposits | Users can hold dollar balances outside banks | Commercial banks, EM deposit bases | Stablecoin issuers, exchanges |

| FX corridors | Stablecoins reduce need for local-currency conversion | FX brokers, prefunding desks | Dollar stablecoins |

The current $7.2 billion in cumulative on-chain crypto-card volume accounts for roughly 2.2% of the $322.6 billion stablecoin market cap, with USDT at $189.2 billion and USDC at $76.6 billion, per DeFiLlama.

Standard Chartered forecasts that stablecoin supply will reach $2 trillion by the end of 2028, while JPMorgan’s more conservative view puts the figure at around $500 billion.

If card spending continues at its current 2.2% share of stablecoin supply, Standard Chartered’s bull case implies roughly $45 billion in annual crypto-card volume. If penetration doubles as rewards programs scale and global card access expands through Bridge’s 100-country rollout, that approaches $90 billion.

JPMorgan’s bear case still implies $11 billion in annual revenue at current penetration. Even the bull scenario sits below 1% of Visa’s current annual payment volume, a ratio that forecloses the displacement argument and reinforces Visa’s consumer front end as stablecoin balances compound.

In the bear case, growth in crypto-card spending slows to around 25% annually as rewards normalize, compliance requirements tighten, and frictions in converting on-chain balances to card-usable fiat prove sticky, leaving annual crypto-card volume at roughly $9 billion.

Visa’s share of that volume would pull toward 75% as Mastercard’s stablecoin infrastructure matures, since the network announced plans to acquire BVNK for up to $1.8 billion and said consumers can already spend stablecoins across over 150 million Mastercard merchant locations.

Stablecoin cards stay a real product, serving crypto-native users who would have held stablecoins regardless, but one that stays peripheral to consumer payments at large.

In the bull case, Jupiter-style programs scale across more blockchains, Bridge’s 100-country expansion delivers genuine volume from emerging markets where dollar-denominated wallets address real FX pain, and user growth compounds off today’s small base, pushing annual crypto-card spend toward $18 billion.

Visa’s 90% share holds or strengthens, implying roughly $16 billion in Visa-routed stablecoin card volume and representing a structural addition to its card-ready balance sourcing, with the acceptance layer wholly intact.

Mastercard’s BVNK acquisition fits the same logic, as both networks compete to become the dominant consumer front end for on-chain balances before those balances outgrow their current niche.

The GENIUS Act disadvantages the anonymous direct-payment model proposed by the original crypto thesis and favors card networks as the natural compliance interface between on-chain balances and consumer commerce.

| Scenario | Annual crypto-card volume | Visa share assumption | Visa-routed volume |

|---|---|---|---|

| Bear case | ~$9B | 75% | ~$6.8B |

| Current run-rate / base | ~$7.2B–$7.8B cumulative reference point | ~90% | ~$6.5B–$7.0B |

| Bull case | ~$18B | 90% | ~$16B |

| Stablecoin supply bull penetration case | ~$45B at 2.2% of $2T supply | Network-dependent | N/A |

| Double-penetration case | ~$90B | Network-dependent | N/A |

Bank deposits, cross-border prefunding, FX corridors, and correspondent banking face direct competition from on-chain dollar balances.

ECB officials cited risks of less stable deposits, reduced bank lending capacity, and complications for interest-rate transmission.

Euro stablecoins account for only 0.3% of the total stablecoin supply, a figure that makes the dollarization risk embedded in global stablecoin adoption. Visa’s position is the checkout terminal, and that is exactly where stablecoin cards hand control back to it.

The actual prize Visa captures is the consumer interface to stablecoin balances as those balances grow from $322 billion toward the $2 trillion projection.

Every dollar of stablecoin supply that routes through a Visa-linked card is a dollar that could have funded a competing payment rail and instead chose the one already embedded in 175 million merchant terminals.

Stablecoins are rewriting cross-border finance while extending Visa’s reach at the point of sale.

The post Stablecoins were supposed to bypass credit cards, but now Visa is winning crypto card payments appeared first on CryptoSlate.

Bitcoin and Ethereum ETFs posted more than $1.4 billion in combined weekly outflows, while money moved into Hyperliquid, XRP and Solana funds. Liquidchain is pitching

Apple’s Siri redesign with AI features could redefine user interaction, potentially setting new standards for voice assistants and AI integration. The post Apple to unveil

The ceasefire deal could stabilize oil markets and influence geopolitical dynamics, but its success hinges on Trump’s approval and nuclear talks. The post US negotiators

Coinbase’s listing of DRV could boost its visibility and liquidity, potentially increasing user engagement and market interest in decentralized derivatives. The post Coinbase lists Derive